So you’ve finally made it: the big, fat seven-figure bank account. 1M! For those who have the privilege of seeing that balance in their account, the thrill is both exhilarating and scary. On the one hand, you are happy to be admitted to the world’s 0.6% club. On the other hand, you are now preoccupied with maintaining and growing your wealth. Understandably, managing 1 million (CHF, EUR or USD) is vastly different from managing 100K.

In this article, you will learn how to manage your 1,000,000 (CHF/EUR/USD) from someone who has had years of experience managing and growing a successful multi-million dollar personal portfolio.

See also:

- Investing 100K: Key principles, opportunities and risks overview

- Investing 200K: How to find satisfactory returns

- Low-risk investments in Switzerland: How to get above-zero returns

The philosophy of wealth

It is important to take a step back and understand what wealth is and what its limitations are.

First of all, wealth cannot buy you time or health (some may even include happiness in this bracket). These are intrinsic to the laws of physics that govern our world. No amount of money, stocks or properties can change this fact.

That being said, wealth is an important facilitator in your life. It allows you to accomplish your objectives with ease and minimal frustration, thus increasing your pleasure. It is also an enabler of interpersonal interaction which enhances your personal well-being.

When viewing wealth as a facilitator (rather than the end goal), the natural question is, “what is the end goal?” Unfortunately, there is no universal answer to this – it is as personal to every individual as a fingerprint. However, by understanding your end goal, you can better appreciate your investment objectives and thereby deploy your capital strategically.

The 4 principles of investing globally and in Switzerland

Books weighing as much as bricks have been written on this subject. There is much technical and academic literature out there, each one fiercely disagreeing with the other. We have distilled them into 4 easy-to-remember principles that are relevant across any investment scenario.

1. Don’t lose money: this is the Number 1 Rule for Warren Buffett and it’s something I hold dearly. Never invest in a venture that has a high risk of permanent capital loss. This refers to projects (or companies) with underlying structural defects that could put them out of business one day, rather than just causing temporary fluctuations in valuation. After all, any percentage gain can be temporary whereas a 100% loss is permanent.

2. Don’t forget Rule #1: the idea of never losing money is so important that it’s worth reinforcing it with a rule of its own.

3. Slow and steady wins the day: here’s a brain teaser. Which investment will yield a greater return: 5% for 10 years, or 10% for 10 years but with a 35% market fall in the middle? Yes, you’ve guessed it correctly, a steady 5% return year on year triumphs. This is a simple mathematical reality: percentage gains and losses are not created equal. A 50% loss will require a 100% gain to return to break even. Always remember that.

4. Self-edification is the only way to survive and thrive: there might be more than a few individuals and firms out there willing to help you “manage” your wealth. The truth, however, is that nobody will place your interests closer to heart more than you will. As a result, it’s vital to educate yourself about investing so that even when you do end up entrusting your capital to a professional, you still have the know-how to keep them on their best behaviour.

The wealth playbook: How to invest 1M

Now that you are well versed with the principles of investing, it’s time to put them into practice. This playbook section will teach you how.

Purpose & Goals

It might sound cliché, but investing without a goal in mind is like sailing to an unknown destination. You won’t know when or if you’ve reached your goal. Consequently, it’s important to know what you want your portfolio to become in the future.

At the most basic level, there are 2 key functions of a portfolio:

1. To generate a sustainable and rising level of income -> this is ideal if you want to live off the passive income stream and achieve financial independence. At the 1 million level, with a 5% yield, you’ll be looking at 50K of income every year, which can propel you towards financial independence.

2. To achieve real growth in the capital value of the portfolio -> this is usually for creating a sizable lump sum for a specific future endeavour (e.g. house purchase, education).

Depending on which goal you pursue, there will be different asset allocation implications. For example, income-focused investors would allocate greater capital to income-generating assets (fixed income, dividend stocks), whereas growth-minded investors would invest in high-potential growth stocks.

Establish your time horizon

Do you want to achieve your goal in 5, 10, 20 or just 2 years? Your time horizon is critical in deciding your asset selection. Generally, the faster you want to achieve a certain goal, the greater the return needs to be and hence the higher the risk. As a result, your time horizon is directly linked to the risk you need to take on.

A good benchmark would be the long-term average return of the Swiss Market Index, which has delivered 5.82% Average Annual Total Return for the past 30 years. At this rate, your portfolio should double in value every 12 years.

The general advice at the 1M level is to just let the portfolio grow by itself, and to interfere as little as possible. This way, you can enjoy the full effect of compound growth and let time do all the hard work.

Choose the right portfolio structure

Should you invest in a tax-advantaged account, via your pension or a general investment account? These might sound trivial, but they make a real and significant difference to portfolio performance, because each will have different tax implications.

There are various tax shelter accounts (Pillar 2 and 3 accounts in Switzerland) set up by governments to encourage people to save and invest. They either have no or deferred tax liability, which will enable your portfolio to grow in a tax-free manner in the interim. Use them!

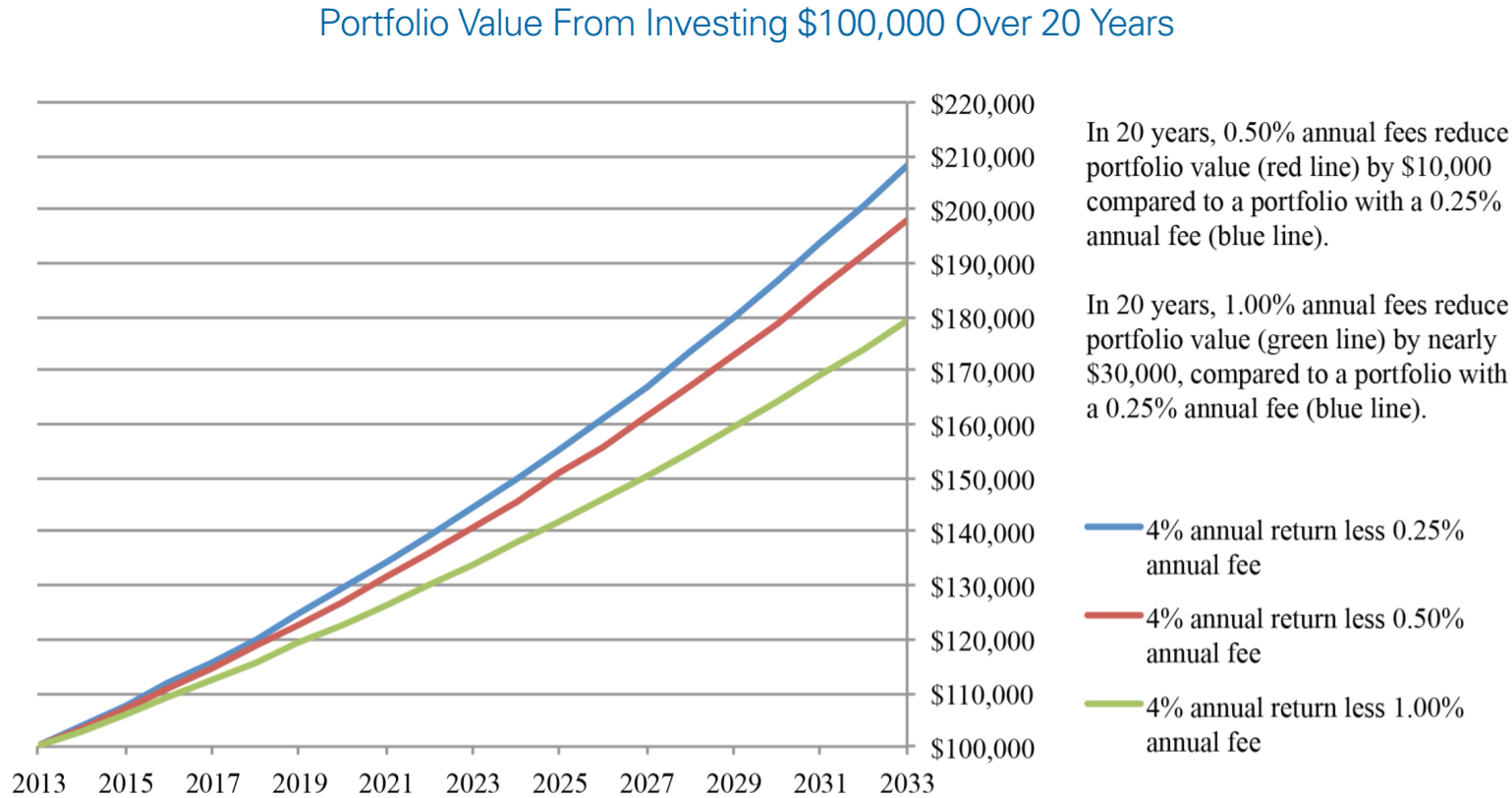

Still oblivious to the effect of taxation on your portfolio? It has been documented that even an additional 1% fee can exert a detrimental drag on long-term portfolio performance. Imagine the effect of a 25% capital gains tax!

Taxes are real expenses that act as drag on your portfolio. Having the right structure will enable your capital to grow in the most tax-efficient manner, allowing you to enjoy the maximum effect of compounding. Even a 1% saving can have a tremendous long-term effect as illustrated above, so choose wisely.

Don’t put all your eggs in one basket

The old saying “never put all your eggs in one basket” remains the key commandment in the investing world, even when investing in Swiss Francs, considered one of the world’s most stable currencies.

Diversification simply means having a selection of assets with uncorrelated risk-reward profiles. For example, adding some gold into an equity-only profile means that when equity takes a bashing, the gold should increase in value (due to its haven asset status). Research indicates that if you place 20 completely uncorrelated assets in a portfolio, then there’s little risk of long-term value erosion, because losses in one would be more than made up by gains in others.

Equally, diversification means constructing a portfolio that is wide-reaching. You may know the local Swiss market inside out, however, it will not help you if EU-Swiss relations break down and all of your assets remain in Switzerland.

By investing in assets across the world, you can mitigate the risk of a specific geography.

Here are 3 easy ways to diversify your asset allocation and geography:

1. Use a multi-manager multi-asset class fund.

2. Purchase a selection of geographical and asset class specific ETFs.

3. Buy an international index fund (e.g. FTSE World Index).

Diversification reduces portfolio volatility and is essential for long-term growth.

A side effect of diversification is portfolio rebalancing. Due to constant changes in the underlying valuation of assets in a portfolio, the optimal asset allocation can never be maintained in the long-term. It is therefore important to periodically adjust (through buying and selling) to return to that optimal allocation. Due to the effort and fees that may involve, it is recommended to rebalance no more than twice a year.

Beware of fees & Costs

We saw the detrimental effect of fees on the long-term performance of a portfolio earlier: a 0.75% fee will reduce the terminal portfolio value by 17% at the end of a 20-year period.

It goes without saying that any measures to minimise fees should be considered. Here are 3 easy-to-remember techniques:

• Use a fixed-fee platform rather than one based on the percentage of the net asset value.

• Use low-cost index funds (fees levied at no more than 0.25% per year) unless the active manager has demonstrated long-term outperformance. Remember, even that can turn sour very quickly as illustrated by Neil Woodford this year.

• Don’t overtrade – once you have invested (presumably using dollar-average), simply fire-and-forget and let the market do all the hard work.

Advisors, wealth managers or DIY?

Once you have reached the 1,000,000 mark, there will be no shortage of experts wanting a slice of your time to advise or manage your wealth. After all, money has the magnetic characteristic of attracting more money.

At some point, you will need to make a decision about the way your portfolio is managed. There are 3 main ways:

1. DIY

2. Wealth manager

3. Advisor

DIY is simple and free. You make all the investment decisions yourself and then execute. Technology has made trading so much easier that private investors today can access professional-level trading tools at a cost slightly more expensive than their morning coffee. The upside is that it is free and you will always have your own best interests at heart.

However, you need to have a good understanding of the market as well as a level head, and you’ll need to devote time to your portfolio. In my opinion, it is the best portfolio management technique because nobody will place a greater interest in you than yourself.

Wealth managers, on the other hand, take over your portfolio and make all investment and trading decisions on your behalf. The upside of this arrangement is that it frees up your time and injects professional expertise into portfolio management. However, this can be an expensive approach (fees start at 1% per year) and their core incentive is really revenue maximisation for themselves rather than seeking the best performance for you.

Advisors sit somewhere in between DIY and wealth managers. They provide professional expertise to advise investors on where and how to make investments. However, the ultimate trading authority lies in the hands of investors, who can accept or disregard such advice. Advisors can be informal in the form of friends, or formal financial advisors regulated by the relevant authorities. Formal advice usually costs $200-$500 per hour.

Always keep some powder dry

There are many qualities of Warren Buffett that contribute to his financial success. First and foremost, it is his patience and willingness to hold large amounts of cash for an extended period of time. Cash is what is known as “dry powder” in investing, because it allows you to put it to use (or “fire it”) when you need to.

Having some spare cash in your portfolio is always good because the nominal value of cash does not change and therefore it acts as a natural hedge that reduces volatility. However, the real advantage of cash comes into play during economic downturns when market fear irrationally depresses the valuation of sound and well-run businesses to below their intrinsic value. At that point, you could purchase these wonderful businesses cheaply, thereby increasing your margin of safety (and hence return). Buffett really understood the importance of this point and that’s why he aggressively bought into Goldman Sachs and Bank of America in late 2008.

Keep some powder dry as you might need it quickly (and it’s better to have it than not)!

Trust yourself & Shut out the noise

There is never a shortage of people who seek to project their opinion as loudly as possible. Unfortunately, in the digitally connected world we live in today, these opinions travel way faster than they need to, filling the time that people need to think for themselves.

My advice is to remove these distractions from your life, deploy what you have learnt about investing and listen to yourself. You understand your own circumstances better than anybody else and if that means running against the herd then do it. After all, nobody has ever lost money by not jumping onto the latest bandwagon.

Investment opportunities to consider

Now that we have a good understanding of the principles and practicalities of investing, we will look at the options available to ensure that 1M works as hard for you as it possibly can. Here is an overview of the asset classes available to investors and their various properties.

| Properties/Asset | Cash deposit | Bond | Equity | Real Estate | Commodities | Private Equity and Venture Capital |

| Overview | Depositing capital in a regulated financial institution in exchange for regular interest payments. | Lending capital to corporations or governments in exchange for regular interest payments. | Direct or indirect ownership of public companies. | Direct or indirect ownership of physical properties. | Direct or indirect ownership of commonly traded raw materials (e.g. gold). | Direct or indirect ownership of private companies or early-stage businesses. |

| Capital gains | Nil | Nil on primary markets; possible on secondary markets | 8-10% per year for an index fund. Significant upside with the right growth model. | 5-6% per year on average depending on the location and property type. | Highly variable. Between -50% to 100%+ depending on the type and timing. | Highly variable, can be 0% or 10x+ of invested capital. |

| Income potential | Between 0-3% pa depending on currency and terms. | Investment-grade bonds trading around 3-5% pa. Junk bonds at 8%+. | 2.5% dividend yield per year. | 3-5% rental yield per year. Highly variable depending on location. | Nil | Nil |

| Risks | No risk if the deposit is within the protected limit (currently CHF 100K per individual per bank) | Adverse financial performance leading to debtors defaulting on the loans. | Adverse financial performance undermines the valuation and threatens dividend payment. | Adverse economic conditions could reduce demand and drive down both price and yield. | Highly volatile and vulnerable to swings in global demand and supply. | High uncertainty in business performance (hence return). High chance of permanent capital loss. |

| Liquidity | High if instantly accessible, otherwise a penalty might be incurred. | Usually high as these loans are publicly traded. | Usually high as these securities are publicly traded. | Usually low as properties are illiquid. Can be partially mitigated through investing in REITs. | Usually high as commodities are publicly traded with transparent pricing. | Low |

| Transaction cost | Nil | Low | Low | Around 3-10% depending on the location. | Low | Around 3-5% of the transaction amount. |

| Management cost | Nil | Low | Low | 1% of the asset value per year. | 1% of the asset value per year. | 1-3% of the asset value per year. |

| Minimum Investment | None | Usually around $1,000 | Usually around $1,000 | At least $20,000 for an entire property or $1,000 for REITs. | At least $50,000 for physical commodities or $1,000 for commodity ETFs. | At least $100,000 |

| Suitability | Suitable as a short-term holding facility for your portfolio dry-powder. Unsuitable in the long term due to the erosion of purchasing power from inflation. | Suitable as an income-generating engine of a portfolio. | Suitable as part of any long-term investment strategy. | Suitable as part of a long-term income generation and value preservation strategy. | Suitable as a short-term portfolio hedge against uncertainty. | Suitable for sophisticated investors not afraid of permanent capital loss of the invested capital. |

Conclusion

1 million is a significant amount of capital, which, if invested wisely with the right objectives and time horizon, can deliver serious returns and propel you towards financial independence. As a summary, we will leave you with 3 principles that we hold dear:

• Simplicity over complexity

• Time is your best friend

• Fees kill returns

Happy investing!