So you’ve finally made it. The big 200,000 (CHF, USD, EUR) balance is sitting in your account after all those years of hard work, thrifty spending, and diligent saving. You’ve just entered the world’s top 5% club. Now comes the big question: How do I maintain my wealth? After all, in Switzerland’s low-interest environment, stuffing your cash under the mattress is a sure way to see its value erode quickly due to inflation.

Investing your cash properly is absolutely vital to propel you towards financial independence.

See also:

- Investing 1M: Key principles, opportunities and risks overview

- Investing 100K: How to find satisfactory returns

- Low-risk investments in Switzerland: How to get above-zero returns

Determine your ultimate goal

It might sound cliche, but investing without having a goal in mind is like sailing to an unknown destination. You end up nowhere on the best of the days. Consequently, it’s vital to know what you want your portfolio to become in the future.

At the most basic level, there are two key functions of any portfolio:

- To generate a sustainable and rising level of income – This is ideal if you want to live off a passive income stream and achieve financial independence.

- To achieve real growth in the capital value of the portfolio – Usually this is for creating a sizable lump sum for a specific future endeavor (e.g. a home purchase or educational goal).

Depending on which goal you pursue, it will have different asset allocation implications. For example, income-focused investors would allocate greater capital to income-generating assets such as fixed income and dividend stocks. Whereas growth-minded investors would invest in high-potential growth stocks in Switzerland or globally.

Set your time horizon

Do you want to achieve your goal in 5, 10, 20 or just 2 years? Your time horizon is critical in deciding your asset selection. Generally, the faster you want to achieve a certain performance, the greater the return needs to be and hence the higher the risk level. As a result, your time horizon is directly linked to your risk capacity.

A good benchmark would be the long-term average return of the Swiss Market Index, which has delivered 5.82% Average Annual Total Return for the past 30 years. At this rate, your portfolio should double in value every 12 years.

Choosing the right structure

Should you invest in a tax-advantaged account via your pension or a general investment account? These might sound like trivial questions but the answer will make a real and tangible difference to portfolio performance because each will have different tax implications.

There are various tax shelter accounts (Pillar 2 and 3 accounts in Switzerland) set up by governments to encourage people to save and invest. They either have no or deferred tax liability, which enables your portfolio to grow in a tax-free manner in the interim.

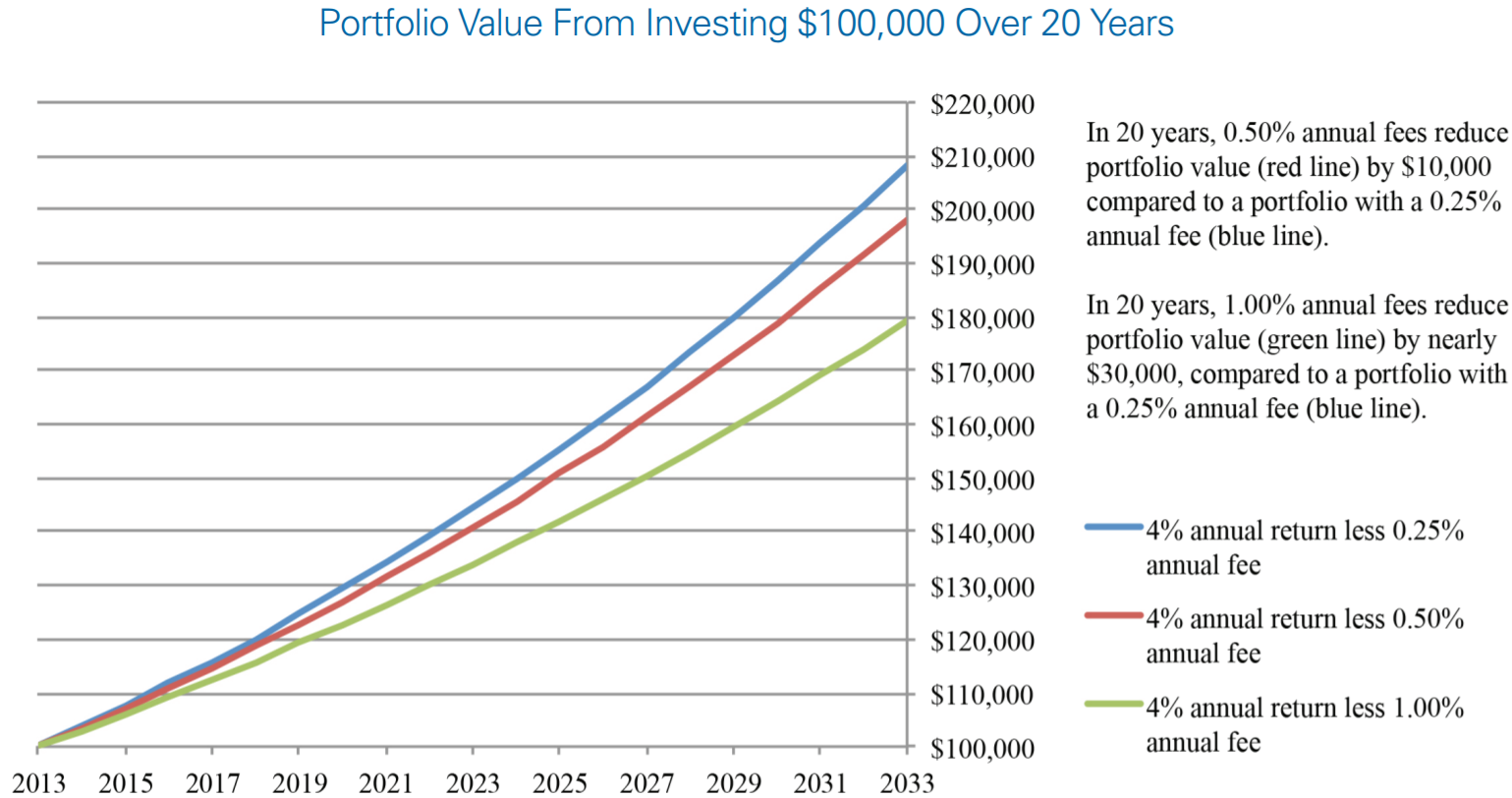

Still uncertain about the effects of taxation on your portfolio? It has been documented that even an additional 1% fee can exert a detrimental drag on long-term portfolio performance. Imagine a 25% capital gains tax!

Diversification is key

The old saying “don’t put all your eggs in one basket” remains the key directive in the investing world.

Diversification simply means having a selection of assets with uncorrelated risk-reward profiles. For example, by adding some gold into an equity-only profile means in times of uncertainty, even though equity might be taking a bashing, the gold should increase in value due to its haven asset status.

Equally, diversification means constructing a portfolio that is wide-reaching. You may know the local Swiss market inside and out. However, it will not help you if EU-Swiss relations break down and all of your assets are in Switzerland. By investing in assets across the world, you can mitigate the risk of specific geography.

Here are 3 easy ways to diversify your asset allocation and geography:

- Use a multi-manager, multi-asset class fund

- Purchase a selection of geographical- and asset class- specific ETFs

- Buy an international index fund (e.g. FTSE World Index)

Diversification reduces portfolio volatility, which is essential for long-term growth.

What does this all mean in practice for a Swiss investor?

To put everything we’ve talked about into perspective, it may be helpful to construct several sample investment portfolios to see how they compare against each other.

| Sample portfolio | Cash portfolio | Equity-bond portfolio | Equity-bond- property portfolio |

Property-

precious metal portfolio |

| Description | 100% cash or cash equivalents (e.g money market funds) | 60% equity index fund + 40% bond fund | 50% equity index fund + 25% bond ETF + 25% REITs | 50% buy-to-let property + 50% physical gold |

| Overall suitability | Suitable if investors wish to take on minimum risk and not be worried about eroding purchasing power due to inflation Key risk is the erosion of purchasing power from inflation. |

Suitable for investors with a minimum 5-year time horizon and who will not need the capital during the period Key risk would be short-term capital value fluctuation. |

REITs tend to be less volatile than equity and bonds, therefore this portfolio is suitable for more conservative investors Key risk is capital fluctuation and decreased liquidity which can happen during the times of extreme market turbulence. |

This is a highly conservative and illiquid portfolio, which is suitable for investors who hold bearish views on the market and who prioritize income and capital security over other factors Liquidity is the main risk to this portfolio. |

| Security tickers | N/A | Equity: global ETF, US ETF Bond: investment-grade corporate ETF |

REIT: Realty Income | Physical gold ETF Property: actual property |

| Income potential | Depending on the currency, from -0.5% to 2% per annum | 2.5% on equity, 4% on bonds, Combined at 3.2% |

2.5% on equity, 4% on bonds, 5% on REITs, Combined at 4% |

5% on property, 0% on gold, Combined at 2.5% |

| Capital potential | N/A | 8% pa for equity, 3% pa for bond, Combined at 6.5% pa |

8% pa for equity, 3% pa for bond, 2% pa for REITs, Combined at 5.5% |

4% pa on property, 0-3% pa on gold |

| Risks | Capital and income risks are negligible as long as the total amount is within the deposit insurance scheme of the country | Equity: both capital and income (dividend) are subject to fluctuation and therefore aren’t guaranteed. Bond: prices subject to change if not bought at issuance and held to maturity. Income (yield) may be subject to the default risk of the underlying operation of the issuer deteriorating |

Equity and bond risks remain the same as before REITs: their underlying asset is usually real estate, whose valuation can be more difficult to ascertain. During times of market distress and when faced with high redemption rate, managers will need to sell these properties quickly to meet investor withdrawal, which impacts pricing |

Both property and gold are physical assets which are highly illiquid. As a result, during times of market distress, it can be difficult to convert them into cash without suffering a substantial drop in valuation |

| Liquidity | High if an account is instantly accessible; otherwise difficult to access without incurring a penalty (or inaccessible) | Usually high and traded on major exchanges | Generally, REITs have high liquidity due to them being traded on exchanges. However, in times of distress, their liquidity will fall because the underlying asset is illiquid | Low |

| Transaction cost | N/A | Low (less than 0.1%) | Low (less than 0.1%) | 1.5-2% |

| Management cost | N/A | ~ 0.5% pa | ~ 0.5% pa | ~ 1.5% pa |

| Stress test during a downturn | The value of the portfolio should remain unchanged as it’s not subject to any market pricing effects | If subject to the effects of the Great Recession, the portfolio nominal value may decrease by 25-30% within the space of a quarter | If subject to the effects of the Great Recession, the portfolio nominal value may decrease by 15-20% within the space of a quarter | If subject to the effects of the Great Recession, the portfolio nominal value may decrease by 10-15% within the space of a quarter |

It is important to note that these are sample portfolios that have not taken the geographical allocation into account. In practice, where you place your assets is equally important. For example, the Swiss property market was barely affected by the Great Recession. Whereas neighboring markets suffered double-digit declines. It goes back to illustrate the importance of keeping a diverse range of assets across multiple countries.

Should you work with a wealth advisor or DIY?

By the time you have reached the 200 000 mark, no doubt all sorts of “financial advisors” and “wealth experts” will be looking to snatch a piece of your time. They’ll all be eager to help you to manage your wealth.

Whilst an entire article (and more) can be written about whether to hand over the control to these experts or do it yourself, here is a quick summary about each approach:

| Approach | Pros | Cons |

| DIY |

|

|

| Professional manager |

|

|

Generally, if you are comfortable with the various terminologies of investment and have a decent understanding of the various asset classes and their respective characteristics, then it is a sign that you may be ready to manage (at least partially) your own portfolio. Otherwise, it may be better to use a professional manager who is compensated by the hour. Just be sure that they do not receive commissions from the underlying funds in your portfolio.

In conclusion

Others may tell you that investment strategy is too complex for the average investor. Yet it’s true that universal, underlying principles are extremely simple:

- Set your goal

- Determine your risk capacity

- Choose the right structure

- Diversify

- Let time do the magic

Compare it to nurturing an oak tree. It can be painfully slow initially, but once the roots have taken hold, almost nothing can tame its growth. Like the great oak, investing can also be a slow process that yields massive results over time.