Back in the 1920s, following the defeat of World War One, Germany went through radical changes. The empire was over but a new German republic rose from the ashes.

For a time, it looked like millions of middle-class families would quickly rebuild their lives. In no small part because Germans are such diligent savers. But the money they hoarded, before and during the war, soon became almost worthless.

The Treaty of Versaille put the nail in the coffin of Germany’s chances of making a swift post-war recovery. A severe economic crisis struck and the Great Depression took hold. Hyperinflation then wiped out the wealth of most German savers who held the Reichsmark.

But luckily there was another cohort of German savers, who, having foreseen the trouble posed by the Treaty of Versaille, actively shifted their assets out of the country and into neutral countries like Switzerland. There they employed professional wealth managers to look after it for them.

So this small group of wealthy Germans not only correctly predicted financial meltdown, but due to expert asset management, actually saw their wealth increase.

The main takeaways from this story are:

- You should never leave all your wealth in one country (just like never putting all your eggs in one basket)

- Wealth managers not only protect but also enhance your wealth

We will focus on the role of wealth managers in this article.

What is a wealth manager?

A wealth manager, as the name suggests, is someone who professionally manages wealth, in order to meet the financial goals of clients. In today’s world, this often includes liquid wealth, (i.e. cash, bonds, shares) but can extend to all other aspects, like properties, private equity, and venture capital.

This role differs from that of a financial advisor. The latter offers a holistic view of the client’s overall financial affairs, (which ranges from wealth to tax, insurance, debt management, and estate planning) whereas the former focuses exclusively on maintaining and enhancing wealth for clients.

Wealth managers organise themselves into wealth management firms, which usually fall into three camps:

- Full-service private banks: traditional banks seeking to extend their services to high-net-worth individuals and typically require a minimum liquid asset of $3M.

- Financial service companies: large financial firms that offer insurance, annuities and wealth management services.

- Independent advisors: smaller firms with specific niches and target sectors.

As expected, large firms focus on the breadth of service and try to be all-inclusive, whereas smaller companies are specialists. It is therefore not surprising that smaller companies tend to outperform the market by 1.5% per year, as they have the expertise and flexibility to deploy capital effectively.

Essentially, wealth management is the consultative process of meeting the needs and wants of affluent clients, by providing appropriate financial products and services.

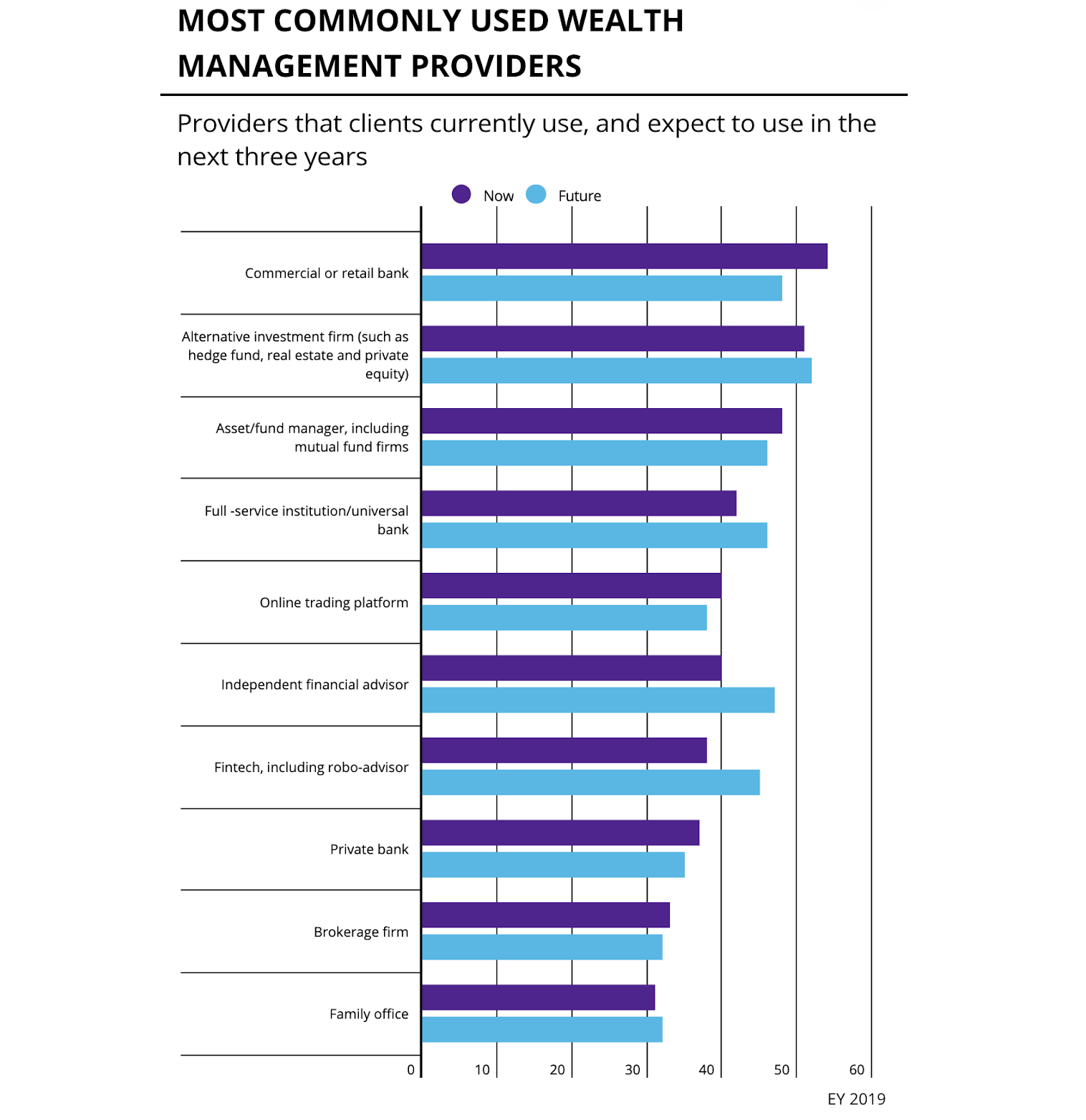

Traditionally wealth management services are provided in person. However as seen in Figure 1 below, there are two key trends that are brewing in the sector, thanks largely due to technology changes:

- Non-banking players are entering the market: these include firms like robo-advisors as well as online trading platforms. This is possibly due to the erosion of trust in banks amongst the public as a result of the Great Recession.

- Service can be provided remotely: with the likes of robo-advisors not just entering but also quickly gaining market shares, the traditional ways of wealth management are being disrupted and replaced by a virtual world, opening up a whole new client base.

Figure 1. The emergence of new players in the wealth management market.

Source: Raconteur

Where is the wealth manager located?

Wealth managers are located throughout Switzerland and broadly speaking, they fall into one of these three categories:

- Local: possess the best knowledge of local trends (e.g. property market and canton tax) and usually provide personal and intimate services.

- Regional: usually specialists with sought-after skills (e.g. green energy sector investment).

- National: typically private banks with national branch coverage for the convenience of their clients.

It is likely that most wealth managers will only take on a limited number of clients. This is for two reasons. Firstly, it ensures the ultimate in professional quality service. Secondly, licensed wealth managers need to register with the local financial regulators, if they take on more than five clients.

Why are wealth managers useful?

Wealth managers can provide four primary benefits to clients when used properly.

- Help create a viable long-term financial plan

People are evolutionarily conditioned to think short-term. Yet investment requires the opposite mentality. As a result, having an unbiased third party to create a long-term financial plan can add tremendous value and maximise wealth enhancement. - Minimise financial stress by judiciously executing plans

It is one thing having a plan but without proper execution, it is merely a nice looking piece of paper (or PDF). Wealth managers are trained to execute financial plans unemotionally, thus ensuring they are deployed as intended. - Access investment opportunities unavailable to general public

Do you ever wonder why you never got the chance to invest in Uber or Facebook when they were infant companies? Well, because these investment opportunities were not public to begin with. They were private placements that only a handful of intermediaries (e.g. wealth managers) had access to. They were hidden gems. Consequently, if your investment style is adventurous, having a well-connected wealth manager with a fresh “deal flow” can be invaluable. - Work with tax specialists to minimise tax liability

Tax is a fact of life. However, tax also exerts a major drag on portfolio performance. We already know the difference 1 percentage point makes on the long-term return prospect of a portfolio. Imagine 20%! Having a wealth manager who can work with tax specialists to minimise your tax bill is a treasured trait.

Here is a list of services commonly offered by wealth managers. It is important to note that the quality of services offered varies rather wildly. It is critical to examine the credentials and experience of anyone calling themselves a wealth manager..

- Investment management and advice, including retirement planning

- Legal and estate planning

- Accounting and tax services

- Examination of health care and social security benefits

- Charitable giving plans

- Help with starting or selling a business

How to choose the right wealth manager?

There’s a wide array of wealth managers on the market, all with different qualities, styles, and experiences. Choosing the one that fits your needs and budget can be the difference between a stress-free encounter and grudging frustration.

At the heart of the matter lie two critical factors:

- Does the wealth advisor have the relevant skills and experience to manage your wealth?

- Does the wealth advisor have the right incentive and moral compass to put your best interests at the heart of every decision he makes?

Basically you should perform your own due diligence on your prospective wealth manager. What we have discovered is that, by asking a series of control questions (identical questions across multiple recipients), you can begin to develop a preference of one wealth manager over another.

- What is your professional accreditation in wealth management?

- Describe your typical client

- Are you a registered investment advisor?

- Are you affiliated with any financial brokers?

- Does your firm offer proprietary funds or separately managed accounts?

- Does your firm receive any third-party compensation for recommending particular investments?

- What is your investment philosophy?

- Will my money be ring-fenced in a protected account?

- How frequently will we meet?

- What is your charging structure?

By asking the same 10 questions to several different wealth managers, you will be able to gauge responses and decide which ones you want to speak further with, and which ones you do not.

How do wealth managers make money?

Wealth managers are compensated in three key ways:

- Time spent servicing clients

- An annual management fee based on the percentage of the asset under management

- Commission from recommending investment products

Out of these three routes, the annual management fee is by far the most common route, as it is both scalable and profitable for wealth managers. The cost of managing a CHF 1 million and CHF 100 million portfolios is very similar, because all transactions are electronic these days. Yet the latter will extract 100 times more revenue than the former. The current market rate is between 1-2% per year.

Time spent servicing clients is another route, which is based on the hourly rate of the wealth manager performing services on behalf of clients. This can range from CHF 250 to 400 per hour. Some firms can adopt a hybrid approach incorporating both the time spent and the management fee model.

As a general rule, you should avoid wealth managers who adopt the commission model, because they are incentivized to sell you investment products rather than advising on your best interest.

When to run away from your wealth manager?

You may think that your wealth manager has your best interest at heart. The reality may be more unsettling. To many, their first interest will always be selfish – their own financial interest. They will then work with you around this parameter.

Here are five obvious red flags, which if a wealth manager displays, should make you consider swiftly moving your money elsewhere.

- Receives commission for recommending certain investment products: this means they definitely do not have your interest at the heart of their decision-making process. You should question the suitability of every product they ever sold you.

- Manages the portfolio passively: you might as well put your money in an index fund. Remember, you are paying for the performance.

- Charges more than 2% of your portfolio size every year: most likely you are no better off by investing the fund passively as very rarely can wealth managers consistently achieve a 2% outperformance.

- Poor track record: this one is pretty obvious.

- Bad service: if you don’t have a good personal rapport, you won’t be getting the best service, so what hope for your investment?

The judgement call

Selecting a professional and unbiased third-party to look after your wealth is a critical exercise of personal judgment.

Perform due diligence. Make sure you establish trust and a personal rapport, but always check their credentials are unblemished first. You’ll know when you found the right one.

Because the best wealth managers not only take a lot of the weight off your shoulders. It can also be extremely liberating and rewarding to watch your portfolio being professionally managed and enhanced.

More importantly, it will give you the precious commodity of time. The key is to ensure your interest and that of your manager are as closely aligned as possible.