Imagine waking up late on a typical working day without worrying about being late for work. Instead, you gradually clamber out of bed and meander down the road toward your favourite cafe. And there you chill with a delicious smoothie and watch the world go by over a leisurely lunch.

You’d probably get fired if you did this and had a regular job, but you don’t have to worry because a decent-sized deposit just landed in your bank account from the castle you co-own in Aargau. And since it is more than sufficient to cover your living expenses, you are suddenly blessed with an ample supply of the most precious commodity on earth. Time.

The above isn’t some pipe dream enjoyed by billionaires but achieved by many mortal souls around the world. Such individuals have decent-paying professional jobs but they also save and invest diligently, often in assets that produce steady and regular passive incomes.

For example, by putting money in crowdfunding, you can become a co-owner of a purpose-built student building in a prime university campus located in the UK. And it may not only earn a handsome yield (when compared to the paltry rates offered by banks) but also offer excellent potential for capital growth.

In fact, despite enjoying ultra-low interest rates since the Great Recession, investors seeking alternative assets were often unable to secure enough venture capital, due to the continuing lack of liquidity in major banks.

As a result, intermediary platforms began to spring up, which connected and amalgamated retail investors to property developers and thus the real estate crowdfunding market was born.

What is real estate crowdfunding?

Crowdfunding, like any form of funding, simply provides capital for a specific venture. However, crowdfunding differs from traditional investing because the number of participants is much larger. As a result, specific platforms exist to match the crowd (i.e. individual investors) with businesses/projects which require funding. Such platforms also handle the administrative, legal and accounting side of investing on behalf of investors. Their revenue derives from either a commission from successful funding and/or annual management fee levied on investors. There are several types of crowdfunding which are explained here.

How does real estate crowdfunding work?

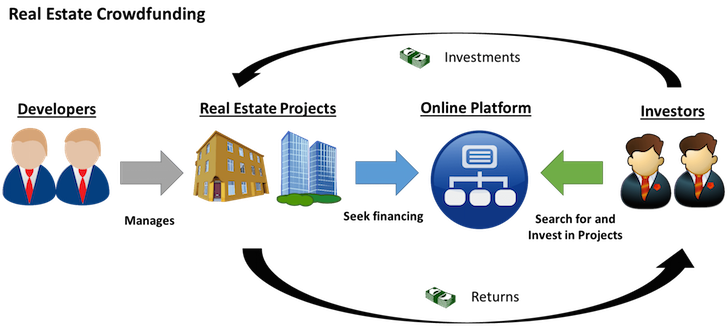

Figure 1 below is a simple illustration of real estate crowdfunding. At the centre is the crowdfunding platform, which matches developers seeking finance for their projects with investors willing to commit capital. These investments can be in the form of both equity or debt. The investment platform levies a fee on developers and/or investors.

Figure 1. The mechanism of real estate crowdfunding

Source: Financial Samurai

Crowdfunding and the traditional approach

Traditionally, investing in the real estate market includes several complicated stages encompassing the bidding and acquisition phases, usually followed by a period for renovation or refitting. Eventually, the asset is primed for renting or selling. It is a cumbersome process that exerts pressure on the investor. Crowdfunding is slightly different because it is a hands-off process. Investors simply commit capital and outsource the rest to the platform. Here we compare the two approaches below.

| Factor | Traditional RE investment (direct ownership) | Crowdfunding RE investment |

| Initial capital outlay | At least CHF 100,000 | Starting from as low as CHF 500 |

| Asset availability | Usually limited to residential apartments and houses | High – can be residential, commercial as well as industrial |

| Asset class | Investors are limited to the equity tranche | Investors can choose both the equity and debt tranches |

| Geographical reach | Most investors choose to buy in areas they know well (i.e. locally) | Platforms offer properties from across the country |

| Transaction cost | Around 1% of the purchase amount | Around 1-2% of the purchase amount |

| Third-party costs | Bank transfer fees may be applicable | Depending on the platform, some may charge an initial fee of up to 1% |

| Management cost | It depends on the type of management involved. DIY can be performed cheaply whereas 3rd-party management often takes up to 15% of the total gross rent. | Managed professionally and it costs around 10% of the total gross rent. |

| Management effort | Medium to high | Low |

| Income potential | Yields 3-6% depending on the amount of leverage | Yields 3-6% depending on the amount of leverage |

| Capital appreciation | Yes | Yes, if invested in the equity tranche |

| Capital risk | Subject to market performance | Subject to market performance. Debt investors may suffer from default risk. |

| Liquidity | Low as property takes time to sell | Low to medium. Some platforms offer a secondary market to trade. Others may offer buyback programs after a specific time period. |

| Leverage | Up to 60% loan-to-value ratio | Indirectly – the investor could invest in the equity tranche of the project. |

An overview of different crowdfunding platforms in Switzerland

There are several different players in the Swiss market, but for serious investors, a range of objective and quantitative tests ought first be performed to ascertain suitability.

Based on publicly available information we look at each platform from the following angles.

- Asset type and availability – what can I invest in?

- Minimum investment amount – can I afford it?

- Fees and charges – how much non-investment capital will I lose?

- Liquidity – can I get my money back easily?

- Profitability – what was the average ROI?

- Income frequency – how often will I receive an income?

- Reporting type and frequency – how will I be kept informed of my investment?

| Factors | Crowdhouse | Crowdli | Foxstone | MyBrick |

| Asset type | Majority residential with a small amount of commercial (usually attached to the apartment) | Exclusively residential | Exclusively residential | Exclusively residential |

| Asset class | Equity | Equity | Equity

Debt |

Equity |

| Min. amount (CHF) | 100,000 | 10,000 | 25,000 | 25,000 |

| Fees | 3% initial fee + 3% to 5% annual management fee based on gross rent | 4% initial fees + 4% annual management fee based on gross rent | 3% initial fee + 0.05-0.25% annual management fee based on property value for equity

3% from investors and 3% from developers for debt |

2-3% initial fee + an undetermined annual management fee |

| Liquidity | Sales take on average between 36-90 days | No clear answer provided except “investment time horizon advised being between 7 and 10 years” | Equity resale can happen at any time. Debt needs to be held to maturity | Equity resale can happen at any time as long as a willing buyer can be found |

| Return on equity | 4-7% | 5-7% | 4-7% | 5-8% |

| Income | Paid out monthly | Paid out quarterly | Paid out quarterly | Paid out quarterly |

| Money-back guarantee | No | No | No | Only if the campaign was terminated by myBrick |

| Reporting | Monthly | Quarterly | Quarterly | Quarterly |

A deep-dive into Swiss crowdfunding platforms

1. Crowdhouse

Website: www.crowdhouse.ch

Minimum investment amount: CHF 100,000

Crowdhouse started off as a crowdfunding property investment platform but in recent years diversified into real estate brokering. It offers 3 primary business streams:

- Buying a property outright (either as owner-occupier or investor)

- Buying a partial stake in the property (as an investor, starting from CHF 100,000)

- Selling a property to Crowdhouse

It searches, locates, negotiates and organises the purchase on behalf of investors as well as performing the legal and administrative formalities associated with managing properties. Investors’ details are entered into the Swiss Land Registry in order to demonstrate legal ownership. Charges are based on an initial fee (3%) and annual management fee (3-5% per year). This represents a fairly expensive drag on the portfolio and investors need to be sure of the return prior to committing the capital.

2. Crowdli

Website: www.crowdli.ch

Minimum investment amount: CHF 10,000

Crowdli is a traditional crowdfunding platform that matches investors to property sellers. The platform levies a 4% property management security charge as well as a 4% initial transaction cost to investors, which we consider to be exceptionally high. Its return is primarily in the form of quarterly dividends (between 5-10%) although it does advise a 5-7% return on equity per year. It does not appear to offer a short-term liquidity option as it advises investors to keep the investment for between 7 to 10 years.

3. Foxstone

Website: www.foxstone.ch

Minimum investment amount: CHF 25,000

Foxstone was established in 2017 as a platform that enables crowdfunding for real estate acquisition and crowdlending for property development. Investors can choose to deploy their capital as equity to acquire and become co-owners in properties. This enables them to benefit from rental income and any potential capital appreciation on the horizon. Alternatively, investors can choose to invest in bonds issued by the platform on behalf of property developers, which pay out a fixed interest rate quarterly until maturity.

The initial fees for both equity and debt tranches stand at 3% and investors will be liable for management charges should they choose the equity route. The business is in its nascent stage therefore the selection of property is quite limited (9 in total at the time of writing).

4. myBrick

Website: www.mybrick.ch

Minimum investment amount: CHF 25,000

myBrick was also established in 2017 with the founding ethos of democratising property investing. It focuses on the equity/co-ownership model where investors can benefit from both rental yield and capital appreciation. Its property pool is extremely limited (3 in total at the time of writing) and its fees are slightly cheaper than its competitors. The company acts as a facilitator during the exit, when it assists in the finding of a buyer, rather than having any buyback schemes in place.

Is real estate crowdfunding a good investment?

The short answer is “yes”.

The long answer, unfortunately, like many other open-ended questions on investment, is very much “it depends”.

It very much depends on the investor objectives and overall portfolio composition. Investors with heavy exposure to stocks, bonds and other financial assets often look to real estate as a sensible portfolio diversification play. As an alternative asset class, it also offers a good hedge against adverse market conditions. That said, investing in Swiss property funds can achieve a similar objective, albeit at lower cost and much higher liquidity.

Where real estate crowdfunding really shines is the ability to handpick projects that suit requirements. Most platforms have a diverse range of opportunities with different risk-return profiles, so you can choose the ones that fit your needs and disregard the ones that do not. This is something that cannot be achieved in REITs.

Furthermore, the legal structure of crowdfunding is much simpler than REITs and investors tend to be direct shareholders in the property and thus have greater influence. An added benefit is that being a private placement, there are no open markets and thus daily valuations do not exist.

However real estate crowdfunding has some serious drawbacks. Firstly each platform reviewed above levies pretty hefty fees. It is not unimaginable to see a portfolio value reduced by 6-8% within the first year, just from fees alone. This means an investment would need to be making at least that much just to stay even.

Secondly, the quality of the platform needs to be carefully studied to ensure it is reputable (and won’t take your money and run). Lastly, this is a pretty new asset class and little research has been performed on its long-term performance.

So far, most of the platforms have raised venture capital to fund growth and operations, so it remains to be seen whether this is a viable business model in the long run.

Looking ahead

Real estate as an asset class has a proven track record of delivering healthy returns for investors. In addition, crowdfunding vastly opens the accessibility of this asset class to ordinary investors and helps them to diversify their holdings. However, it is important to note that such convenience comes at a cost. With hefty initial fees often approaching 4% as well as double-digit annual management fees, such platforms are far from golden goose material yet.

It is why many investors are now zooming in on non-public projects. These are private placements in companies with a proven track record of profitability yet sail under the radar. These hidden gems can often vastly exceed expectations and deliver superior ROI, whilst ensuring the security of capital. All that being said, investors should carefully ponder over their asset mix and only opt for diversification when they identify assets that not only represent a level of risk well below the pain threshold but also spell potential for a pot of gold.